IndiGo Q1 profit drops 20% as airspace closures and weaker yields impact performance

- Net profit dropped 20% YoY to ₹2,176 crore in Q1 FY26; revenue up 5% to ₹20,496 crore.

- Airspace restrictions and weaker travel demand lowered load factor to 84.6% and yields by 5%.

- IndiGo continues cost control measures, returning 16 damp lease aircraft and streamlining fleet.

IndiGo reported a 20% year-on-year (YoY) decline in net profit for the quarter ending June 2025, due to geopolitical unrest, airspace closures, yield pressure, and increased non-fuel costs impacting its performance. The airline reported a net profit of ₹2,176 crore, which is slightly below Bloomberg’s estimate of ₹2,262 crore. Their total revenue from operations reached ₹20,496 crore, showing a 5% increase year-on-year, but it still fell short of the expected ₹20,886 crore.

External disruptions hit airline Ops

IndiGo’s financial results were affected by a series of external disruptions. In May, domestic traffic took a hit following the terror attack in Pahalgam and airport-related restrictions, while the closure of Pakistan’s airspace forced longer flight paths and triggered high cancellation rates, especially on routes to Gulf and European destinations. By June, fresh unrest in the Gulf, sparked by the Israel-Iran conflict, caused further disturbances to international schedules. These factors were compounded by seasonally low travel demand, forcing airlines to reduce fares and, in turn, affecting unit revenue or yields.

Despite these headwinds, IndiGo continued to expand capacity, with Available Seat Kilometres (ASKs) rising 16.4% YoY and Revenue Passenger Kilometres (RPKs) up 13.5%. However, as demand growth lagged behind capacity addition, the airline’s load factor fell by 2.1 percentage points to 84.6%.

Revenue and yield pressure

The combined impact of route disruptions and fare reductions led IndiGo’s yield (the average revenue earned per passenger per kilometre) to fall by 5% year-on-year to ₹4.98. Consequently, the airline’s Revenue per Available Seat Kilometre (RASK) declined by 10% year-on-year, indicating that despite increased flight operations, the airline generated lower earnings per seat.

Cost pressures and mitigation

While fuel costs fell by 9% to ₹5,832 crore, IndiGo faced a sharp rise in core operating costs. Non-fuel Cost per Available Seat Kilometre (CASK) increased 2.5%, rising from ₹2.86 in Q1 FY25 to ₹2.93 in Q1 FY26. This rise was caused by higher employee costs, increased maintenance and repair expenses, higher airport charges, and growing depreciation, all of which put extra pressure on the airline’s profitability.

To offset some of these cost pressures, IndiGo undertook strategic steps, including the return of 16 aircraft on damp lease, a costlier leasing model that includes crew, maintenance, and insurance. These aircraft were originally inducted to meet short-term capacity needs. Their return contributed to a reduction in aircraft and engine lease rental costs, which fell from ₹624.1 crore in Q1 FY25 to ₹492.5 crore in Q1 FY26.

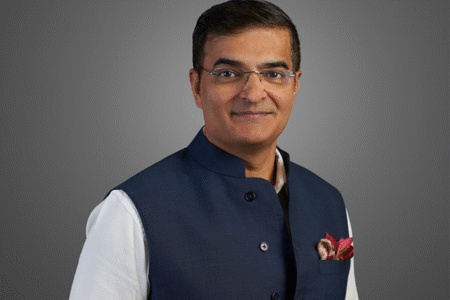

“We have reduced some of the leases, which has helped us financially, even though it doesn’t directly affect the balance sheet. With fewer aircraft on ground (AOG), we’ve also had to rely less on damp leases,” said Pieter Elbers, CEO of IndiGo. “This aligns with our focus on achieving the capacity guidance we have set for the fiscal year.”

Elbers further noted that airspace restrictions significantly impacted operations. “The airspace clearly has disallowed us from operating certain routes. There are 2–3 stations in Central Asia which had to be temporarily suspended, and some routes in the Middle East now require longer circumnavigation. This has impacted our financial results. We had to cancel around 170 flights a day following Operation Sindoor,” he said.

Operational metrics

Passenger demand, though slightly moderated, stayed strong with 31 million passengers flown in the quarter, marking a 12% YoY increase. IndiGo’s available seat capacity grew by 16% to 42.3 billion ASKs, but the load factor declined by 210 basis points, highlighting the gap between capacity and actual demand.

“With the drop in AOGs now in the 40s range, we’ve gained some operational headroom,” Elbers added. “We are also operating fewer damp leases, helping us financially while ensuring we live up to our capacity guidance.”

As of June 30, 2025, IndiGo operated a total fleet of 416 aircraft, comprising 28 A320 CEOs (including 2 on damp lease), 187 A320 NEOs, 141 A321 NEOs, 48 ATRs, 3 A321 freighters, 2 B777s (on damp lease), 6 B737s (on damp lease), and 1 B787 (on damp lease). This reflects a net reduction of 18 passenger aircraft, consistent with the airline’s decision to optimise fleet costs while enhancing reliability.

IndiGo operated a peak of 2,269 daily flights during the quarter, including non-scheduled services. Its network footprint remained expansive, with 91 domestic and 41 international destinations covered.

For the second quarter of FY26, IndiGo expects capacity growth in ASKs to be in the mid- to high-single digit range compared to Q2 FY25. With geopolitical risks still a factor, and competitive fare environments continuing to shape the market, IndiGo’s emphasis appears to remain firmly on fleet optimisation, cost discipline, and agile capacity management.

Read More: India’s Aviation Boom: Emirates, IndiGo, and Global Carriers Battle for Market Dominance